set.seed(123)

n <- 100

x <- runif(n, 0, 10)

y <- 5 + 2*x + rnorm(n, 0, 2)

simdata <- tibble(x, y)Lab 5: Simple Linear Regression

Week 14

Plan

In this lab we will practice:

- Visualizing linear relationships

- Estimating and interpreting simple linear regression models

- Computing slope and intercept manually and using R

- Evaluating model fit (R²) and residuals

- Reflecting on prediction vs. causality

Textbook Reference: JA Chapter 17

Warm-up & Review

Think about:

- What does the slope represent in a regression line?

- Does correlation imply causation?

- Why do we square residuals in OLS?

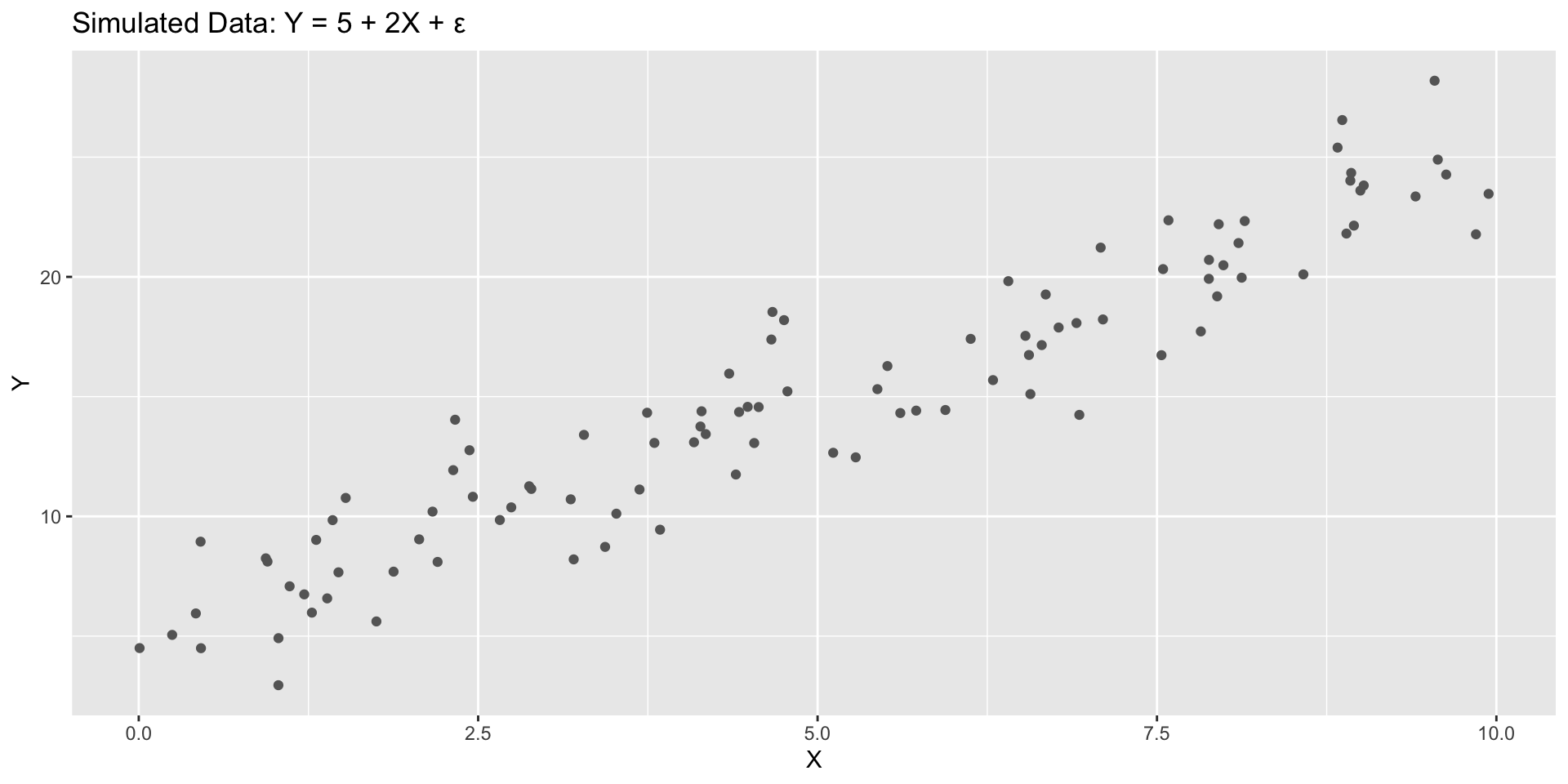

Exercise 1: Visualizing a Linear Relationship

Simulated data

Exercise 1: Visualizing a Linear Relationship

ggplot(simdata, aes(x=x, y=y)) +

geom_point(color="grey40") +

labs(title="Simulated Data: Y = 5 + 2X + ε",

x="X", y="Y")

Task 1

Caution

- What sign do you expect for the correlation between

xandy?

- Add a fitted line using

geom_smooth(method="lm")and confirm visually.

Exercise 2: Manual OLS Estimation

Compute slope and intercept manually using formulas:

\[ \hat{\beta} = \frac{\sum_i (x_i - \bar{x})(y_i - \bar{y})}{\sum_i (x_i - \bar{x})^2}, \qquad \hat{\alpha} = \bar{y} - \hat{\beta}\bar{x}. \]

beta_hat <- cov(simdata$x, simdata$y) / var(simdata$x)

alpha_hat <- mean(simdata$y) - beta_hat * mean(simdata$x)

c(alpha_hat, beta_hat)[1] 4.982080 1.982034Exercise 2: Manual OLS Estimation

Compare with R’s built-in estimator:

model_sim <- lm(y ~ x, data = simdata)

summary(model_sim)

Call:

lm(formula = y ~ x, data = simdata)

Residuals:

Min 1Q Median 3Q Max

-4.4759 -1.2265 -0.0395 1.1927 4.4345

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 4.98208 0.39211 12.71 <2e-16 ***

x 1.98203 0.06836 28.99 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.939 on 98 degrees of freedom

Multiple R-squared: 0.8956, Adjusted R-squared: 0.8945

F-statistic: 840.6 on 1 and 98 DF, p-value: < 2.2e-16Task 2

- Interpret the slope: what does a one-unit increase in \(X\) imply for \(Y\)?

- How close are your manual and R estimates? Why are they identical (up to rounding)?

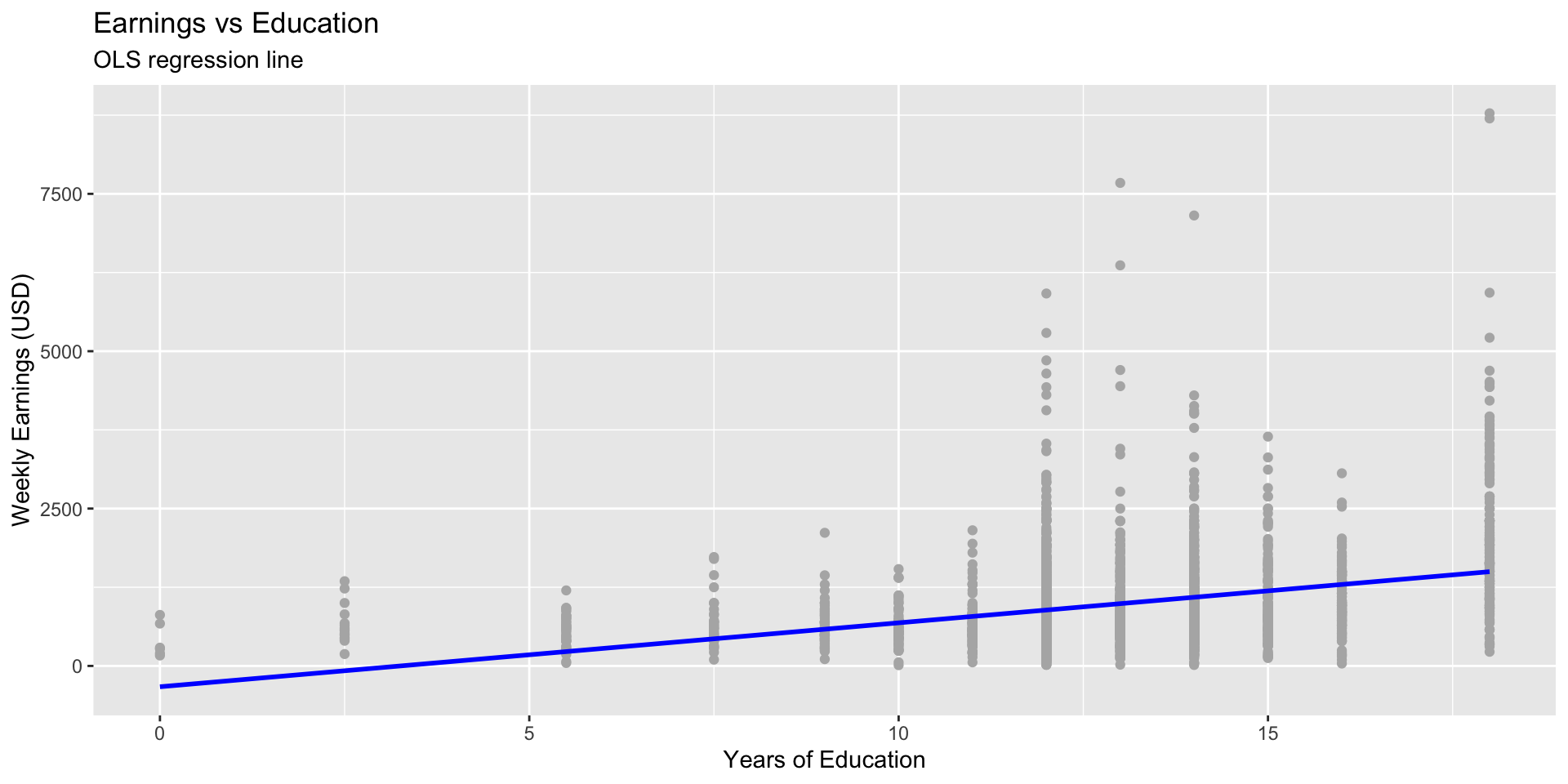

Exercise 3: Regression with CPS Data

Question: How does education relate to weekly earnings?

data(cps)

model_cps <- lm(earnwk ~ educ, data = cps)

summary(model_cps)

Call:

lm(formula = earnwk ~ educ, data = cps)

Residuals:

Min 1Q Median 3Q Max

-1272.1 -417.3 -157.4 229.1 7282.6

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -330.753 72.713 -4.549 5.63e-06 ***

educ 101.550 5.575 18.217 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 709.8 on 2807 degrees of freedom

(1204 observations deleted due to missingness)

Multiple R-squared: 0.1057, Adjusted R-squared: 0.1054

F-statistic: 331.9 on 1 and 2807 DF, p-value: < 2.2e-16Task 3

- Interpret the slope: how much does weekly earnings increase per year of education?

- Is the intercept meaningful here?

- Report \(R^2\) and explain what it measures.

Exercise 4: Visualizing the Fit

ggplot(cps, aes(x=educ, y=earnwk)) +

geom_point(color="grey70") +

geom_smooth(method="lm", se=FALSE, color="blue") +

labs(title="Earnings vs Education",

subtitle="OLS regression line",

x="Years of Education", y="Weekly Earnings (USD)")

Task 4

- Add residual lines with

geom_segment().

- Identify one observation with a large positive and one with a large negative residual.

- What could explain them?

Exercise 5: Prediction and Causality

Use the fitted model to predict average earnings for 12, 14, and 16 years of education.

predict(model_cps, newdata = data.frame(educ = c(12, 14, 16))) 1 2 3

887.8488 1090.9491 1294.0494 Task 5

- What happens to predicted earnings when education increases by 2 years?

- Can we interpret this as a causal effect of education on income? Why or why not?

- What omitted factors might bias the estimate?

Challenge Problem

Simulate a new dataset where \(Y = 5 + 2X + U\) but \(U\) is correlated with \(X\) (e.g., U <- 0.5*X + rnorm(n)).

Estimate the regression again and compare the slope.

Question: Does the estimated slope still recover the true value 2? Why not?

Exit Question

Under what condition can we interpret the slope \(\hat{\beta}\) as a causal effect?

Submission

Submit the rendered PDF or HTML report on Canvas as a group.

Be sure to include your plots, coefficient outputs, and short written interpretations.