Model of Continuous Random Variables

Week 8

Oct 08, 2025

Plan

In today’s class we will learn commonly used models for continuous random variables:

- Normal random variables

- Log-normal random variables

- Chi-square random variables

- Exponential random variables

Textbook Reference: JA 11; SDG 5.6, 8.2

Continuous random variables

- Discrete r.v.: take on countable set of values (0,1,2,…).

- Continuous r.v.: can take on any value in an interval.

- Described by a probability density function (pdf) \(f(x)\) such that:

\[

P(a \leq X \leq b) = \int_a^b f(x) dx

\]

- \(f(x)\ge 0\) for all \(x\), and \(\int_{-\infty}^{\infty} f(x) dx = 1\).

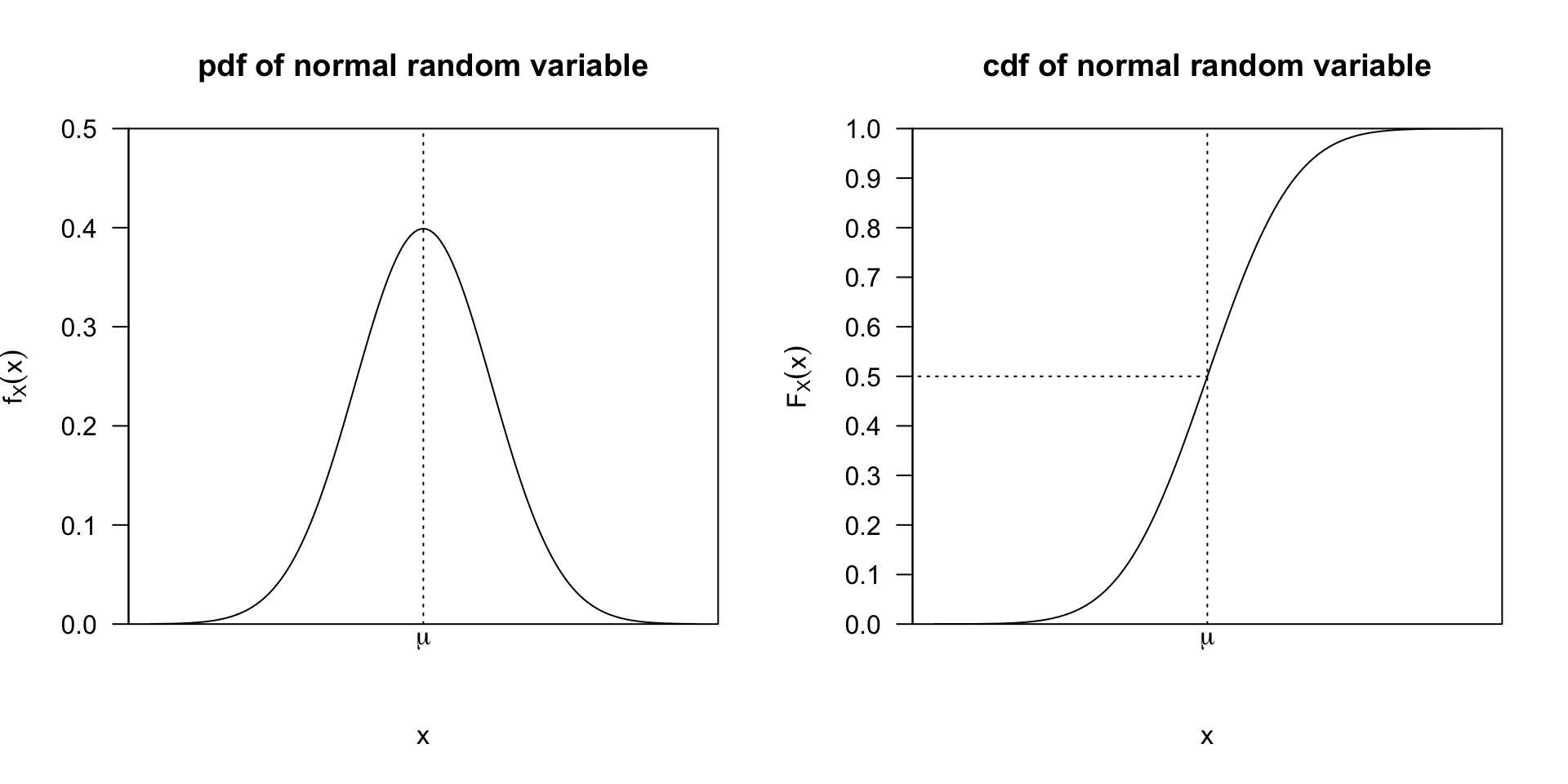

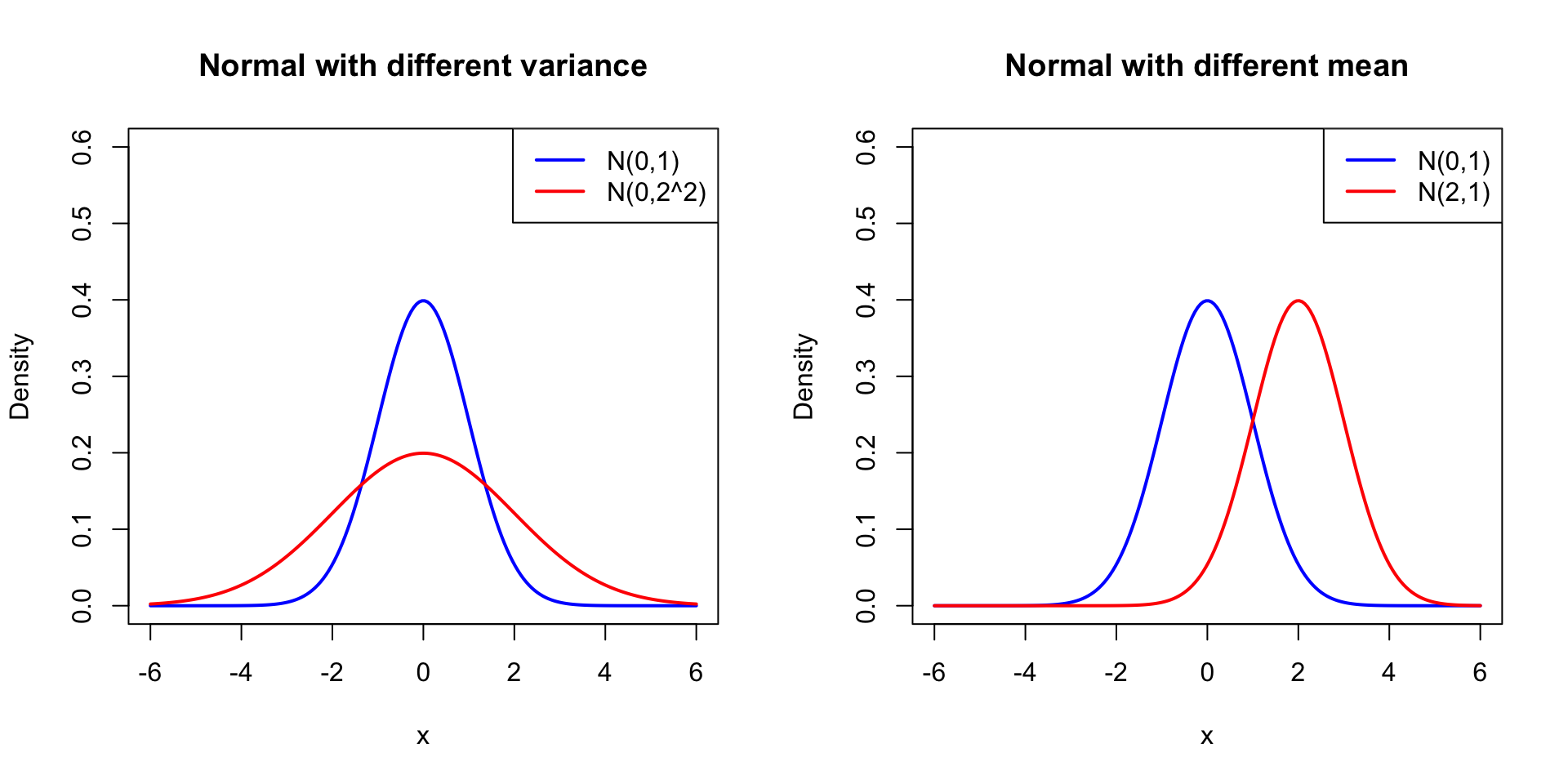

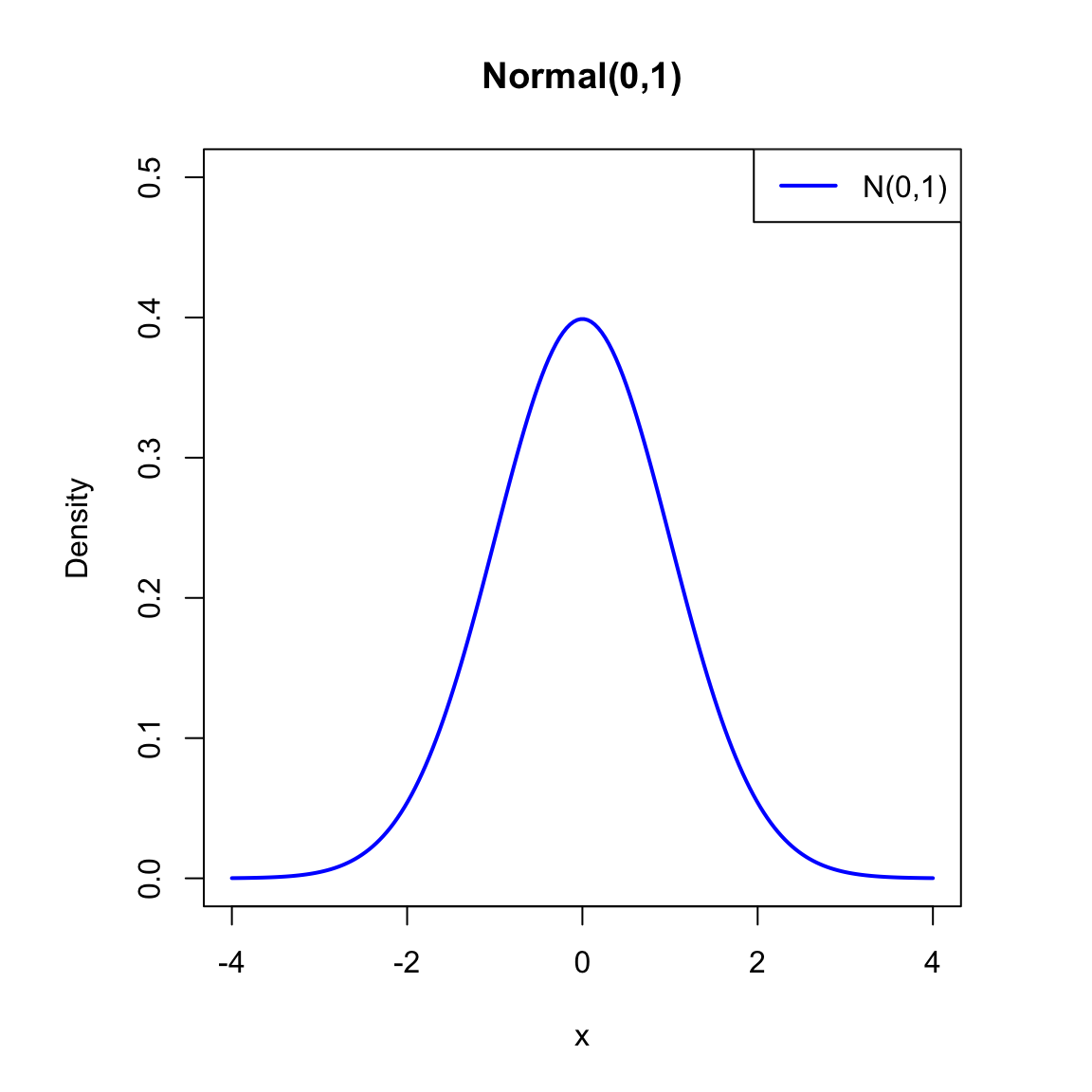

Normal random variables

A random variable \(X\) has a normal distribution with mean \(\mu\) and variance \(\sigma^2\), written \(X\sim N(\mu,\sigma^2)\), if its pdf is

\[

f_X(x|\mu,\sigma^2) = \frac{1}{\sqrt{2\pi\sigma^2}} \exp\left(-\frac{(x-\mu)^2}{2\sigma^2}\right).

\]

- Symmetric around \(\mu\), and has a bell-shaped curve.

- Parameters: mean (\(\mu\)) and variance (\(\sigma^2\)).

- Functions in R:

pnorm(x,mu,sd) # P(X <= x)

qnorm(p,mu,sd) # quantile at probability p

dnorm(x,mu,sd) # density at x

rnorm(n,mu,sd) # random draws

Normal random variables

![]()

Normal random variables

![]()

Normal random variables

![]()

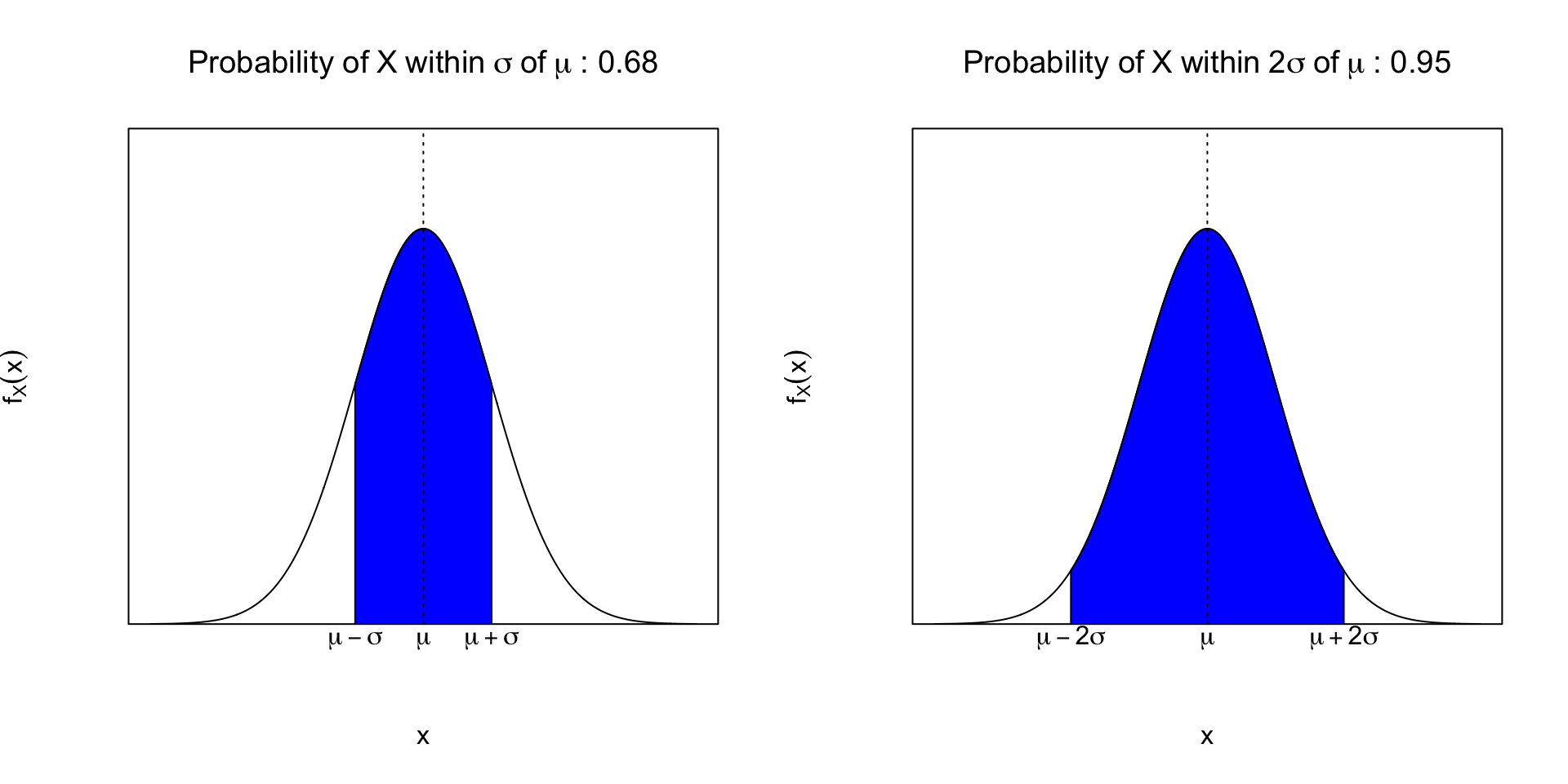

Standard normal

- If \(X\sim N(\mu,\sigma^2)\), then \(Z=\frac{X-\mu}{\sigma}\sim N(0,1)\).

- A standard normal pdf denoted \(\phi(z)\) and cdf denoted \(\Phi(z)\)

- Typically used in probability tables/software. \[P(-1.96\leq Z\leq 1.96)\approx 0.95\] \[P(-1.645\leq Z\leq 1.645)\approx 0.90\]

- Functions in R:

pnorm(z) # P(Z <= z)

qnorm(p) # quantile at probability p

dnorm(z) # density at z

rnorm(n,mu,sd) # random draws

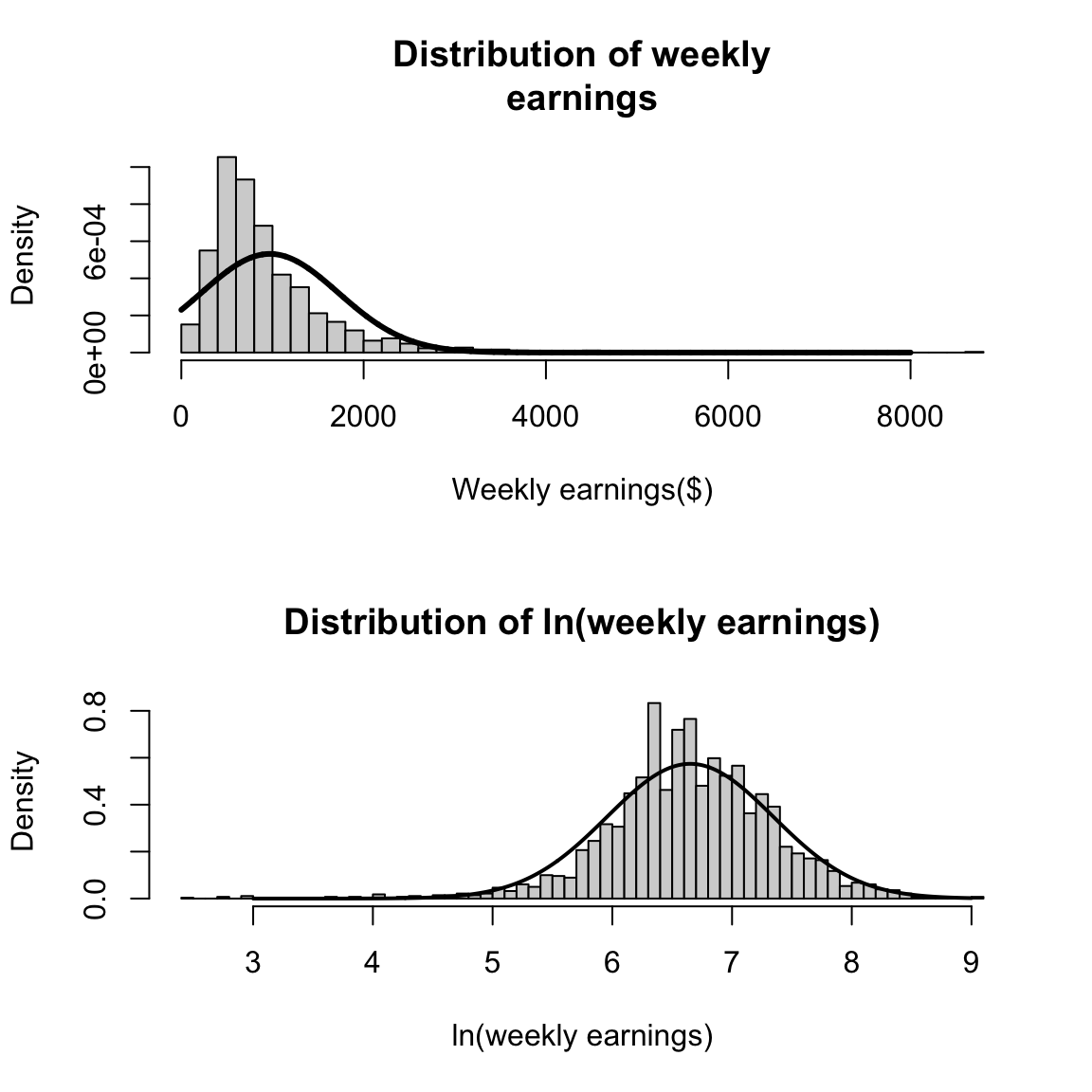

Log-normal random variables

If \(\ln X\sim N(\mu,\sigma^2)\),

then \(X\) is log-normal.

\(X\) only takes positive values.

Skewed right, long tail.

Useful in economics for modeling income, wealth, firm size

Functions in R:

plnorm(x,lnmu,lnsd) # P(X <= x)

qlnorm(p,lnmu,lnsd) # quantile at probability p

dlnorm(x,lnmu,lnsd) # density at x

rlnorm(n,lnmu,lnsd) # random draws

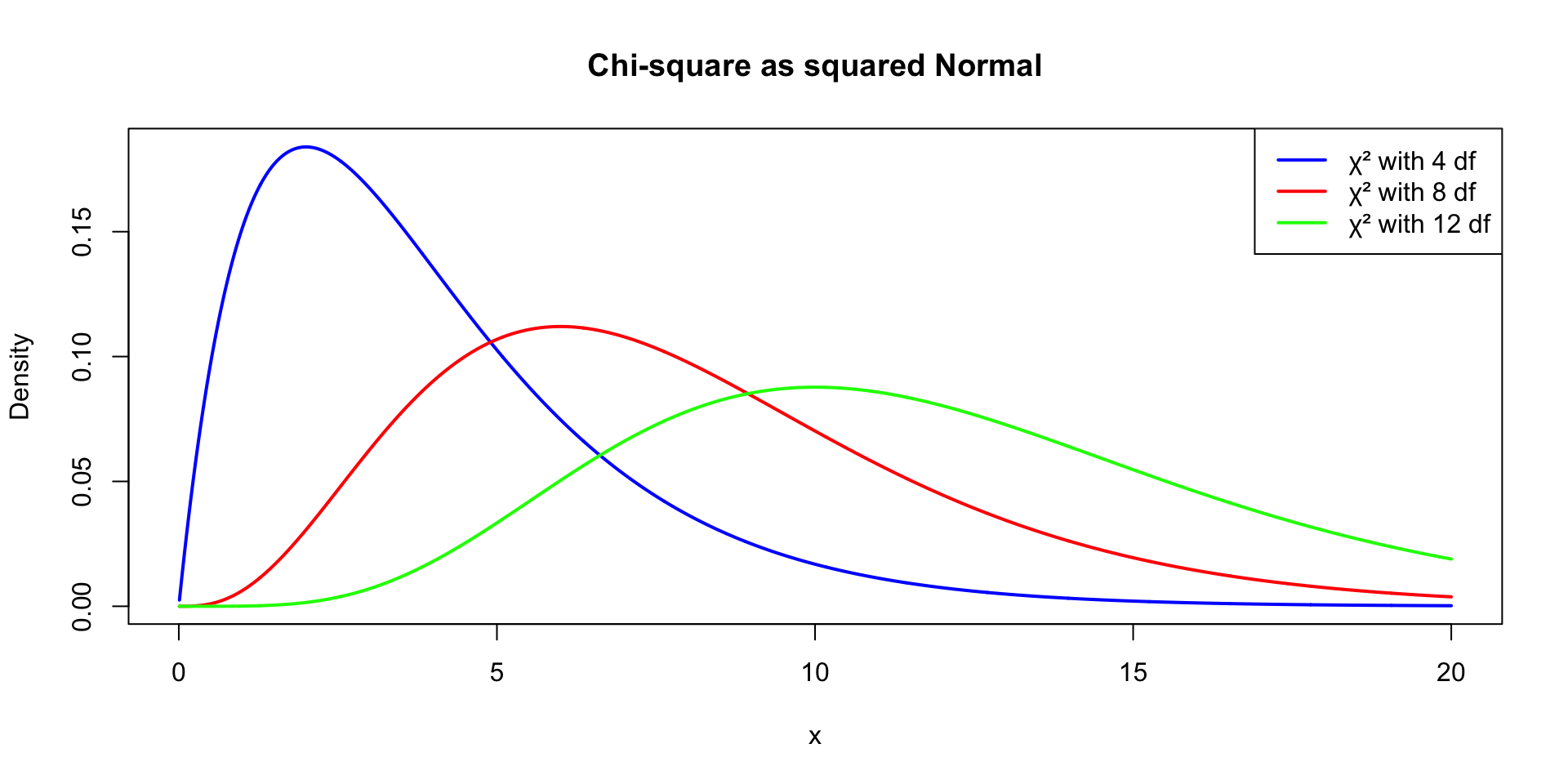

Chi-square

- If \(Z \sim N(0,1)\), then \(Z^2 \sim \chi^2_1\).

- More generally, if \(Z_1, Z_2, \ldots, Z_k \sim\) i.i.d. \(N(0,1)\), then

\[

X = Z_1^2 + Z_2^2 + \cdots + Z_k^2 \sim \chi^2_k

\]

- Key relationship: The chi-square distribution is built from the normal.

- Parameter \(k\) = degrees of freedom.

- Mean = \(k\), variance = \(2k\).

- Used in testing (goodness-of-fit, variance tests).

- Function in R:

pchisq(x,df), qchisq(p,df), dchisq(x,df), rchisq(n,df).

Chi-square

![]()

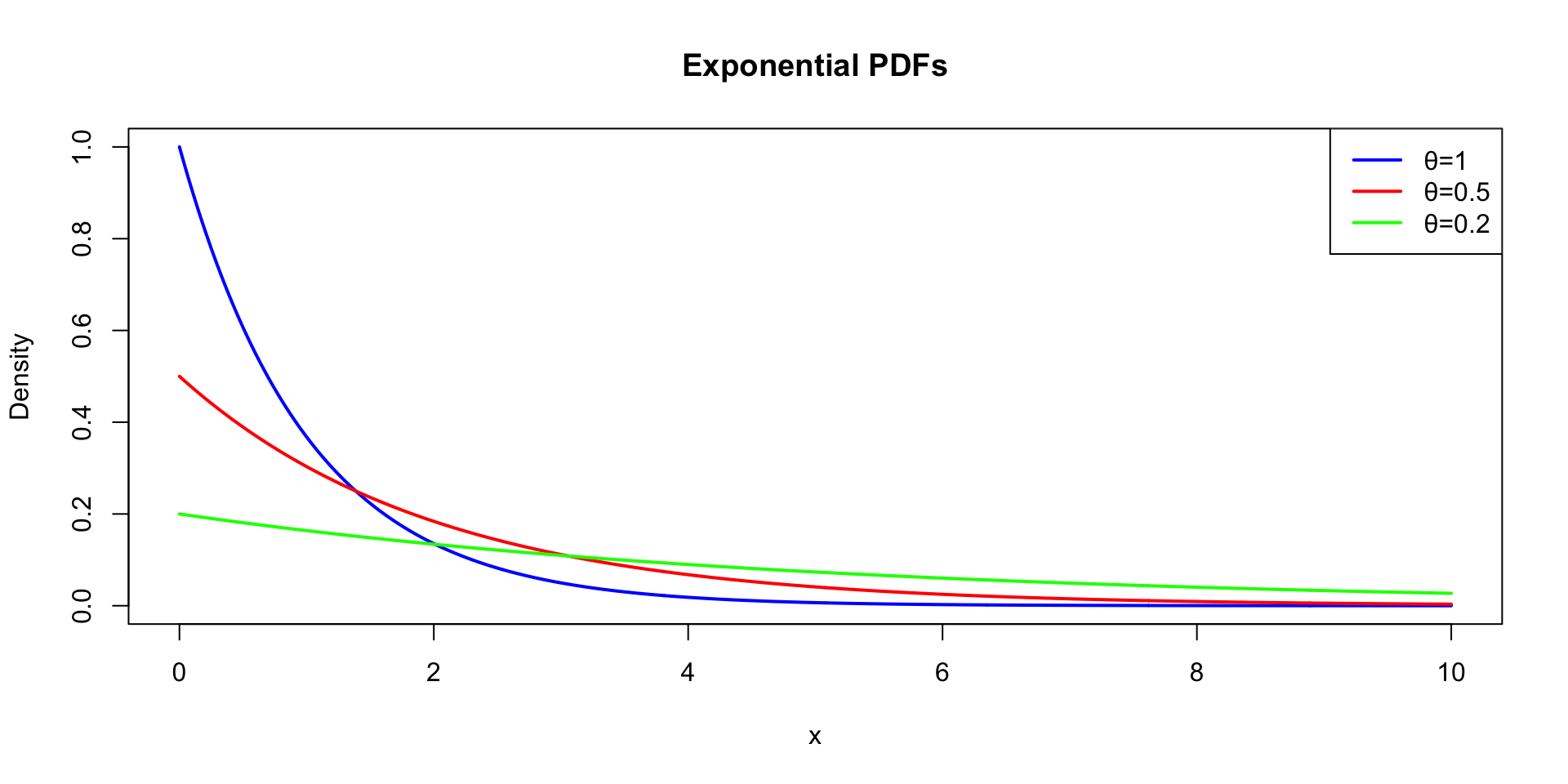

Exponential random variables

A random variable \(X\) is Exponential (\(\theta\)) if:

\[

f_X(x|\theta) = \theta e^{-\theta x},\quad x\ge 0

\]

- Mean = \(1/\theta\), variance = \(1/\theta^2\), CDF: \(F_X(x)=1-e^{-\theta x}.\)

- Applications:

- Duration of unemployment spells

- Time until a trade is executed

- Machine lifetimes

- Function in R:

pexp(x,rate), qexp(p,df), dexp(x,df), rexp(n,df).

Exponential random variables

![]()

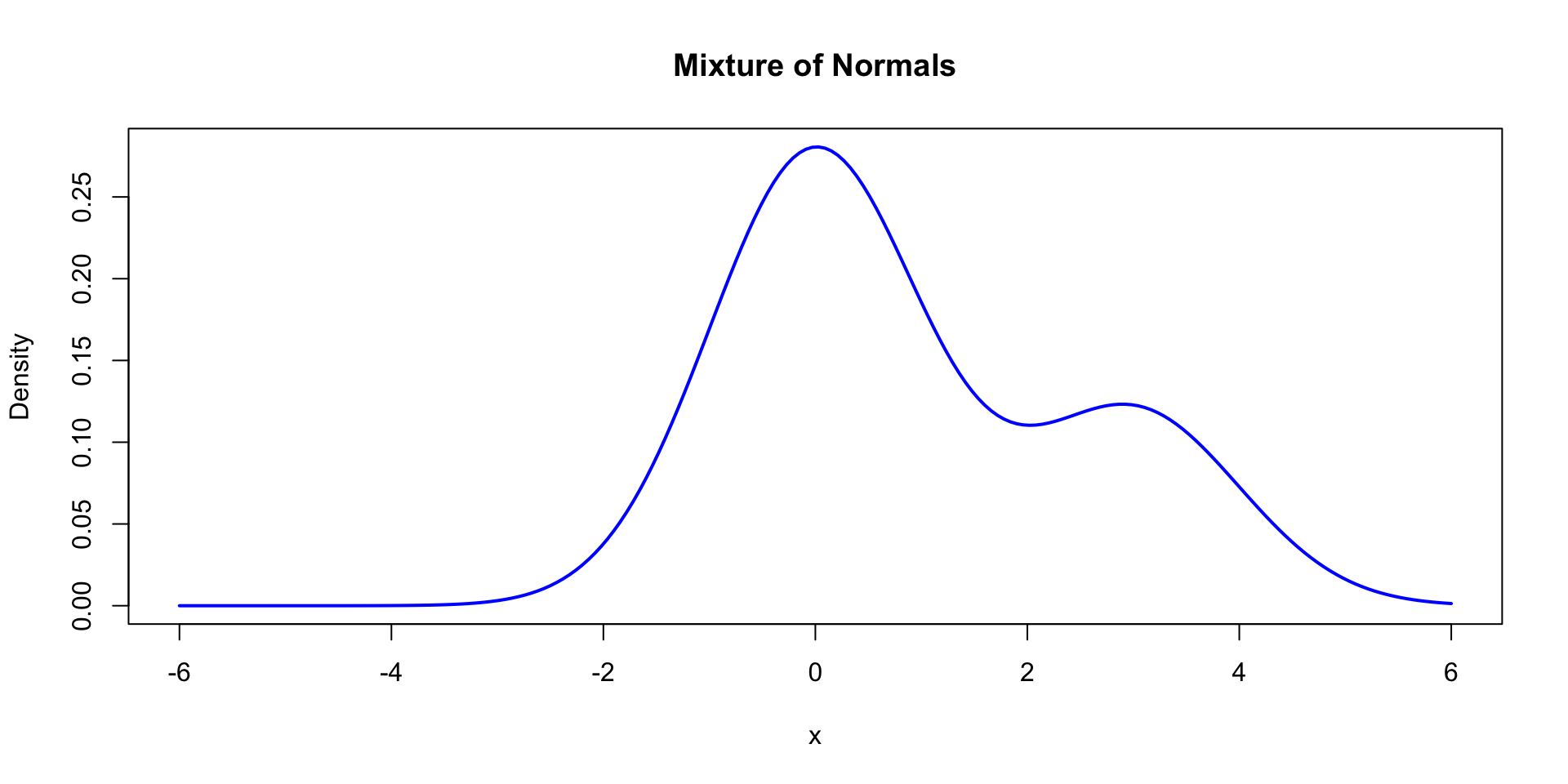

Mixtures of normals

- Some data look “normal-like” but with multiple peaks.

- A mixture of normals is a weighted average of normal distributions.

Economic example: distribution of daily sales may differ between weekdays and weekends.

![]()

Summary

We learned continuous random variable models:

- Normal: symmetric, bell-shaped, most common.

- Lognormal: positive, skewed, used for income/wealth.

- Chi-square: sums of squared normals, variance testing.

- Exponential: time durations, memoryless.

- Mixtures: flexible for multimodal data.