Lab 4: Hypothesis Testing

Week 12

Nov 03, 2025

Plan

In today’s lab, we will practice:

- Conducting and interpreting one- and two-sample t-tests

- Performing one- and two-sided tests manually and using built-in R functions

- Simulating Type I error rates

- Applying asymptotic (z) tests for large samples

Textbook Reference: JA Chapter 14 & 16

Lecture Slides: Hypothesis I, Hypothesis II

Quarto markdown file (.qmd) for today’s lab available on Canvas Module

Best Costume: Louvre Robbers #1 (Charlotte)

Thanks to other characters for participating:

Louvre Robbers #2, Lui*gi Mang*oni, Cat, Hotdogs, Lord Farquaad, Scientist, Hannah Montana, Wizard, Slytherin graduate, Santa Claus (CMIIW Levi??), Anime characters (Jaden).

Let me know if your characters is not mentioned.

Overview

| Test Type | Statistic | Built-in Function | Manual Formula |

|---|---|---|---|

| Two-sided hypothesis | t-stat | t.test(x, mu=c) |

\((\bar{x} - c) / (s_x / \sqrt{n})\) |

| One-sided hypothesis | t-stat | t.test(..., alternative="greater") |

Use one tail of t-distribution |

| Asymptotic (general) | z-stat | manual | \((\hat{\theta}-\theta_0)/se(\hat{\theta})\) |

| Two-sample mean (Welch) | t-stat | t.test(x, y, var.equal=FALSE) |

\((\bar{x}_1 - \bar{x}_2)/\sqrt{s_1^2/n_1 + s_2^2/n_2}\) |

| Two-sample mean (Pooled) | t-stat | t.test(x, y, var.equal=TRUE) |

\(\sqrt{m+n-2}\dfrac{\bar{x}-\bar{y}}{\sqrt{1/m+1/n}\sqrt{s_x^2+s_y^2}}\) |

| Correlation | z-stat | cor.test() |

\((r - \rho_0)/\sqrt{(1-r^2)^2/n}\) |

Submission

- Replicating and submitting pdf worth 70 points, each Task (Try and Reflect/Discuss) worth 5 points, Challenge Problem worth extra 5 points.

- Change the name in the first page to your group member

- Submit the rendered PDF by group on Canvas assignment by Monday 11:59 (Focus on presentation this week)

Warm-up & Review

Recall:

- Null hypothesis (\(H_0\)) vs. Alternative hypothesis (\(H_0\))

- One-sided vs. Two-sided tests

- Type I error (\(\alpha\)) and p-values

Warm-up:

In your own words, what does “reject \(H_0\) at the 5% level” mean?

Warm-up & Review

Recall:

- Null hypothesis (\(H_0\)) vs. Alternative hypothesis (\(H_0\))

- One-sided vs. Two-sided tests

- Type I error (\(\alpha\)) and p-values

Think-Pair-Share:

Discuss with your partner one real-world example where a false rejection (Type I error) could be costly.

Exercise 1: Two-sided t-test

Food trucks: Food truck profits were recorded for a total of six weeks:

Data: $1200, $1150, $1300, $1250, $1100, $1200

The weekly profits of a food truck are normally distributed with unknown mean \(\mu\) and variance \(\sigma^2\).

We’re going to test \(H_0:\mu=1000\).

Manual two-sided t-test

x <- c(1200, 1150, 1300, 1250, 1100, 1200)

n <- length(x)

xbar <- mean(x)

s <- sd(x)

# Manual t-test

c <- 1000

alpha <- 0.05

t_stat <- (xbar - c) / (s / sqrt(n))

t_crit <- dt(1-alpha/2, df = n-1)

p_val <- 2 * (1 - pt(abs(t_stat), df = n - 1))

ci_upper <- xbar+qt(1-alpha/2, df = n-1)*s/sqrt(n)

ci_lower <- xbar-qt(1-alpha/2, df = n-1)*s/sqrt(n)

cat(paste0("Sample estimates: mean = ",xbar,", SD = ",s,

"\nt-stat: ",t_stat," , t-crit: ", t_crit,

"\nReject null: ",abs(t_stat)>t_crit),", 95% CI: (",ci_lower,",",ci_upper,")")Sample estimates: mean = 1200, SD = 70.7106781186548

t-stat: 6.92820323027551 , t-crit: 0.22519364107025

Reject null: TRUE , 95% CI: ( 1125.794 , 1274.206 )Built-in function two-sided t-test

x <- c(1200, 1150, 1300, 1250, 1100, 1200)

n <- length(x)

xbar <- mean(x)

s <- sd(x)

# Built-in R function

c <- 1000

t.test(x, mu = c)

One Sample t-test

data: x

t = 6.9282, df = 5, p-value = 0.0009613

alternative hypothesis: true mean is not equal to 1000

95 percent confidence interval:

1125.794 1274.206

sample estimates:

mean of x

1200 Task 1

Try this

Change the hypothesis to \(\mu=1100\) and rerun. How do the t-statistic and p-value change?

Reflect

Does changing the \(c\) alter the direction or just the magnitude of evidence against \(H_0\)?

Exercise 2: One-Sided t-test

Investment opportunity: You are interested in the possibility of buying a business that produces and sells a certain product. By your calculations, the true average of weekly sales would need to be least $10,000 for the investment to be worthwhile. As part of due diligence, you obtain weekly sales figures from the business for 10 randomly chosen weeks.

Data: in thousand dollars

11.2, 10.3, 12.0, 9.8, 11.5, 10.7, 12.2, 11.9, 10.9, 10.5

The weekly sales of a business are normally distributed with unknown mean \(\mu\) and variance \(\sigma^2\).

We’re going to test \(H_0:\mu\leq10\).

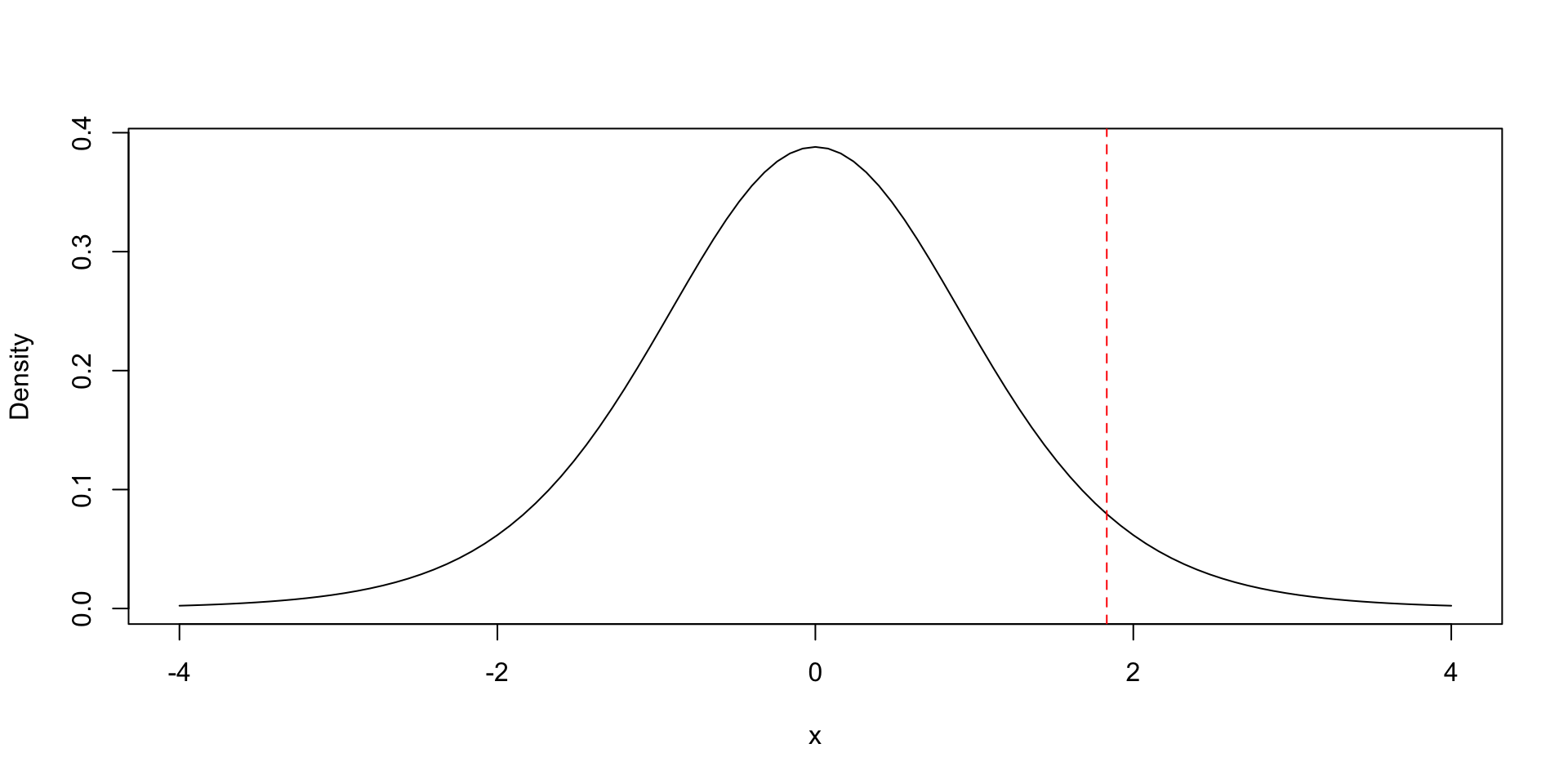

Manual one-sided t-test

Built-in one-sided t-test

sales <- c(11.2, 10.3, 12.0, 9.8, 11.5, 10.7, 12.2, 11.9, 10.9, 10.5)

xbar <- mean(sales)

s <- sd(sales)

n <- length(sales)

# Built-in function: H0: mu <= 10, H1: mu > 10

t.test(sales, mu = 10, alternative = "greater")

One Sample t-test

data: sales

t = 4.3633, df = 9, p-value = 0.0009073

alternative hypothesis: true mean is greater than 10

95 percent confidence interval:

10.63787 Inf

sample estimates:

mean of x

11.1 Visualize rejection region

Task 2

Try this

What would change if the alternative hypothesis were "less" instead of "greater"?

Discuss

Why do we use only one tail of the t-distribution here? How does it relate to directional hypotheses in economics?

Example 3: Simulating Type I Error

Goal: Verify that under \(H_0\), a 5% test rejects about 5% of the time.

Task 3

Try this

Repeat for n = 5, n = 30, and n = 100. Does the rejection proportion stay near 0.05? Why?

Reflect

How does sample size influence the variability of the t-statistic? What does this say about small-sample inference?

Example 4: Asymptotic z-test

set.seed(1)

x <- rlnorm(2000, meanlog = 0, sdlog = 1)

mu0 <- exp(0.5)

z_stat <- (mean(x) - mu0) / (sd(x)/sqrt(length(x)))

p_val <- 2 * (1 - pnorm(abs(z_stat)))

c(z_stat, p_val)[1] 0.7404698 0.4590150

One Sample t-test

data: x

t = 0.74047, df = 1999, p-value = 0.4591

alternative hypothesis: true mean is not equal to 1.648721

95 percent confidence interval:

1.583284 1.793548

sample estimates:

mean of x

1.688416 Task 4

Try this

Try again with only 20 observations. Does the z-test still give a reliable result?

Discuss

Why does the Central Limit Theorem justify z-tests for large samples, even when the data are not normal?

Example 5: Two-Sample Difference in Means

Scenario: Suppose we want to know whether two stores in different cities have the same average daily sales.

Manual two-sample t-test

# Manual two-sample t-test (assuming unequal variances)

mean_A <- mean(store_A); mean_B <- mean(store_B)

sA <- sd(store_A); sB <- sd(store_B)

nA <- length(store_A); nB <- length(store_B)

se_diff <- sqrt(sA^2/nA + sB^2/nB)

t_stat <- (mean_A - mean_B) / se_diff

df <- (se_diff^4) / (((sA^2/nA)^2 / (nA-1)) + ((sB^2/nB)^2 / (nB-1)))

p_val <- 2 * (1 - pt(abs(t_stat), df = df))

c(t_stat, df, p_val)[1] -2.692191151 47.795889615 0.009756215Built-in two-sample t-test

Welch Two Sample t-test

data: store_A and store_B

t = -2.6922, df = 47.796, p-value = 0.009756

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-65.132363 -9.435781

sample estimates:

mean of x mean of y

518.3335 555.6176 Task 5

Try this

Change the sample size to 10 for each store and rerun. What happens to the standard error and p-value?

Reflect

Why might smaller samples lead to more uncertainty about the difference in means? How would equal-variance assumption affect results?

Theory: Equal-Variance Two-Sample t-test

In Example 5, we used the Welch’s t-test, which does not assume equal variances. If we instead assume \(\sigma_X^2 = \sigma_Y^2,\) we can use the pooled-variance t-statistic, often written as:

\[ U = \frac{\sqrt{m+n-2}(\bar{X}-\bar{Y})}{\sqrt{\frac{1}{m} + \frac{1}{n}}\,\sqrt{s_X^2+s_Y^2}}. \]

Equal-Variance Two-Sample t-test

m <- length(store_A); n <- length(store_B)

sX <- sd(store_A); sY <- sd(store_B)

xbar <- mean(store_A); ybar <- mean(store_B)

# Pooled (equal variance) test

U <- sqrt(m + n - 2) * (xbar - ybar) /

(sqrt(1/m + 1/n) * sqrt(sX^2 + sY^2))

p_val_U <- 2 * (1 - pt(abs(U), df = m + n - 2))

# Welch's version

Welch_t <- (xbar - ybar) / sqrt(sX^2/m + sY^2/n)

df_welch <- (sX^2/m + sY^2/n)^2 /

((sX^2/m)^2/(m-1) + (sY^2/n)^2/(n-1))

p_val_welch <- 2 * (1 - pt(abs(Welch_t), df = df_welch))

data.frame(U_pooled = U, p_val_pooled = p_val_U,

Welch_t = Welch_t, p_val_welch = p_val_welch) U_pooled p_val_pooled Welch_t p_val_welch

1 -13.18899 0 -2.692191 0.009756215Reflect

When is the pooled version appropriate? How do results compare with the unequal-variance test when sample sizes or variances differ?

Example 6: Testing Correlation

Goal: Test whether there is a significant correlation between two variables X and Y. We’ll test the null hypothesis \(H_0: \rho = 0\) against the alternative \(H_1: \rho \neq 0\).

First, simulate the data

Using asymptotic z-test

# sample correlation

r <- cor(X, Y)

# Asymptotic variance using sample analog (plug-in)

se_hat <- sqrt((1 - r^2)^2 / n)

# z-statistic and two-sided p-value

z_stat <- (r - 0) / se_hat

p_val <- 2 * (1 - pnorm(abs(z_stat)))

ci_lower <- r - qnorm(0.975)*se_hat

ci_upper <- r + qnorm(0.975)*se_hat

# Display results

cat(paste("Asymptotic z-test for correlation\n","-----------------------------------\n",

sprintf("r = %.4f", r),sprintf(", SE = %.4f\n", se_hat),sprintf("z-statistic = %.3f, ", z_stat),

sprintf("p-value = %.4g\n", p_val),sprintf("CI = (%.4g , %.4g)", ci_lower,ci_upper)))Asymptotic z-test for correlation

-----------------------------------

r = 0.7685 , SE = 0.0018

z-statistic = 419.660, p-value = 0

CI = (0.7649 , 0.7721)Compare to t-test based correlation test

Built-in cor.test() results (t-based)

Pearson's product-moment correlation

data: X and Y

t = 268.53, df = 49998, p-value < 2.2e-16

alternative hypothesis: true correlation is not equal to 0

95 percent confidence interval:

0.7648525 0.7720309

sample estimates:

cor

0.7684658 Task 6

Try this

Generate new samples with weaker correlation (e.g., use Y <- 5 + 0.2 * X + rnorm(n, 0, 2)). Does the correlation remain significant? How big \(n\) should be so that the t-based and normal-based test converge?

Reflect

How does the correlation test relate to slope significance in simple linear regression?

Challenge Problem: Sleep Hours

Question: Do college students sleep less than 7 hours per night?

set.seed(10)

sleep_hours <- rnorm(40, mean = 6.7, sd = 1)

# H0: mu = 7 vs H1: mu < 7

t_stat <- (mean(sleep_hours) - 7) / (sd(sleep_hours) / sqrt(40))

p_val <- pt(t_stat, df = 39)

c(t_stat, p_val)[1] -5.032903e+00 5.644199e-06

One Sample t-test

data: sleep_hours

t = -5.0329, df = 39, p-value = 5.644e-06

alternative hypothesis: true mean is less than 7

95 percent confidence interval:

-Inf 6.529234

sample estimates:

mean of x

6.292324 Challenge Task

Follow-up

- Repeat with

n = 100. - Compare manual and R results.

- Interpret the result in context.

Think

If this were a real study, what confounding factors might affect your inference about student sleep?

Wrap-Up

✅ Key Takeaways

- Always state \(H_0\), \(H_1\), \(\alpha\), and the test direction clearly.

- Manual calculation reinforces understanding; R simplifies application and avoids arithmetic mistakes.

- For large \(n\), t-tests approximate z-tests (asymptotic normality).

- Choice between pooled and Welch t-test depends on whether variances are assumed equal.

- Correlation tests can be done using either t-based or z-based asymptotic methods.

Wrap-Up

| Test Type | Statistic | Built-in Function | Manual Formula |

|---|---|---|---|

| Two-sided hypothesis | t-stat | t.test(x, mu=c) |

\((\bar{x} - c) / (s_x / \sqrt{n})\) |

| One-sided hypothesis | t-stat | t.test(..., alternative="greater") |

Use one tail of t-distribution |

| Asymptotic (general) | z-stat | manual | \((\hat{\theta}-\theta_0)/se(\hat{\theta})\) |

| Two-sample mean (Welch) | t-stat | t.test(x, y, var.equal=FALSE) |

\((\bar{x}_1 - \bar{x}_2)/\sqrt{s_1^2/n_1 + s_2^2/n_2}\) |

| Two-sample mean (Pooled) | t-stat | t.test(x, y, var.equal=TRUE) |

\(\sqrt{m+n-2}\dfrac{\bar{x}-\bar{y}}{\sqrt{1/m+1/n}\sqrt{s_x^2+s_y^2}}\) |

| Correlation | z-stat | cor.test() |

\((r - \rho_0)/\sqrt{(1-r^2)^2/n}\) |

Submission

- Replicating and submitting pdf worth 70 points, each Task (Try and Reflect/Discuss) worth 5 points, Challenge Problem worth extra 5 points.

- Change the name in the first page to your group member

- Submit the rendered PDF by group on Canvas assignment by Monday 11:59 (Focus on presentation this week)

Note

If you want to try different examples, modify sample sizes or change the null hypothesis. Record your findings in a markdown cell for submission.

Feedback form

ECON2250 Statistics for Economics - Fall 2025 - Maghfira Ramadhani